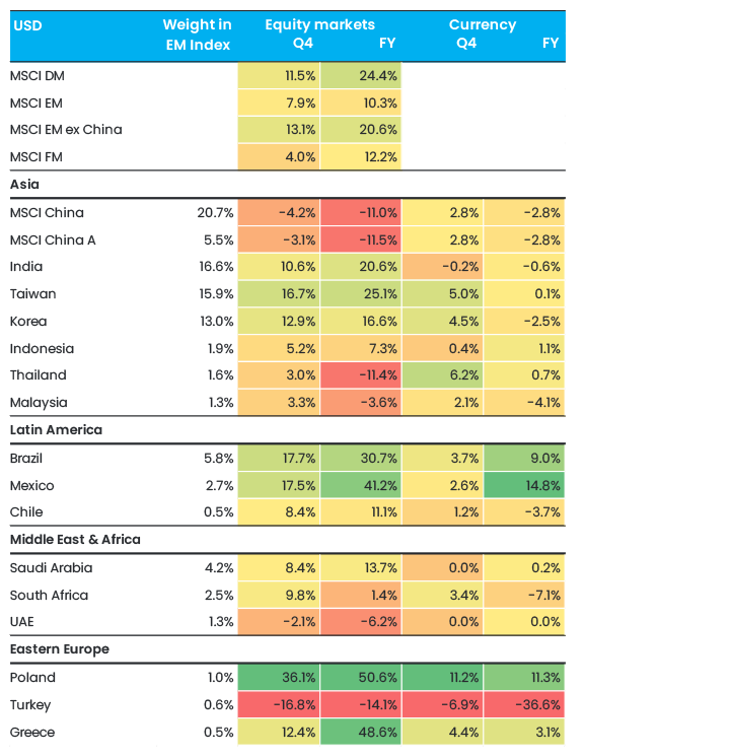

Q4 proved to be a decent end to a remarkably strong year, with emerging markets up 8% in the quarter. Looking at the full year, the 10% return for emerging markets was underwhelming compared with the 24% return in developed markets. However, excluding China, emerging markets returned 21%, which is not too far off the ‘magnificent seven’-driven returns of developed markets. Indeed, most of the best-performing markets in the year were emerging markets, including Poland returning 51%, Greece 49% and Mexico 41% (all in USD).

Figure 1. Equity markets and currency returns in USD

The overriding narrative of 2023 was, of course, US interest rates, with the 10-year treasury yield rising from 3.8% in January to 5.0% in October, before falling back down to 3.9%. These are historic shifts that have profound impacts on both theoretical valuations and spending decisions of consumers and companies, as they directly impact financing costs. This focus on rates will continue into 2024, with the market now pricing in Fed cuts in H1 2024. This would be very positive if it were to happen, as the other big question of the year is how the global economy will cope with this much higher interest rate environment. This week’s World Bank forecast suggests that global growth will be 2.4% in 2024, the weakest since 2009, excluding the pandemic year of 2020. This will be predominantly driven by lacklustre growth in developed countries struggling with high interest rates; advanced economies are expected to grow by 1.2%, compared with 3.9% for emerging and frontier markets. This large discrepancy in growth is a key reason why we believe investors should consider emerging and frontier markets.

The elephant in the room for emerging markets is, of course, China, with MSCI China falling by 11% in 2023. This was due to a raft of well-publicised issues, predominantly centred around the struggling real estate sector. As we wrote in our 2024 Outlook, we do think that the constant drip of government stimulus measures will succeed in stabilising the sector and, hence, that the Chinese economy will recover, albeit at a fairly slow pace. The broader question is how much of this negative sentiment is ‘in the price’. Looking at company valuations, clearly the answer is quite a lot, and we like to use the example of BYD, which recently became the largest electric vehicle producer in the world, overtaking Tesla. BYD has a market cap of USD 80bn and a 2024 P/E of 14x, compared with Tesla’s market cap of USD 744bn and P/E of 62x. However, we accept that, in order to stem the negative sentiment around China, investors will have to see some more tangible signs of improvement and we expect this to take place towards mid-year. In the meantime, we see China as an alpha market and have taken the opportunity to pick up stocks that have sold off significantly despite strong underlying fundamentals. Quite a few of these companies enjoy most of their sales outside China, i.e. they are somewhat insulated from the economic struggles in the country.

The other notable aspect of 2023 was the drastic change in country weights of the MSCI Emerging Markets index; China fell from 32% to 26% in the year, having reached 44% in 2020. India increased to 17% from 8% in 2020, and we think it will continue to grow on strong underlying fundamentals and a buoyant local market with healthy retail flows. This somewhat changes the nature of emerging markets investing, as there is less emphasis on China and more focus on arguably more exciting markets such as India.

Frontier markets ended the year outperforming emerging markets, returning 12%. Even more remarkably, our frontier markets fund returned 24%, in line with developed markets, which is a testament to the strong stock-picking and risk management culture our team has developed. We also note that 2023 was another year when frontier markets had significantly lower volatility (as measured by standard deviation) than both developed and emerging markets, thanks to lower and even negative correlations among individual markets.

It was another busy quarter of travelling for us, with the team on the ground in Mexico, the Czech Republic and Chinese cities including Beijing, Hangzhou, Shenzhen and Shanghai. We also attended the PRI in Person event in Tokyo, where we sat on the organising committee (see our notes on this). Finally, we commenced several significant collaborative engagements in Asia, which we are leading (along with one or two other managers); these include CATL and BYD.

As we highlighted in our 2024 Outlook, despite the remarkably strong returns in 2023, we think 2024 should provide a more favourable and benign backdrop as interest rates start to fall in the US and even more so in emerging markets, especially in countries like Mexico and Brazil, which have some of the highest real rates in the world. Falling rates should also help bring about a slightly weakening USD, which is also typically a trigger for emerging markets outperformance. However, all eyes will very much remain on China. A lot of the bad news is clearly in the price and so, if the government does manage to start to turn the real estate sector around by mid-year, we would expect somewhat better performance than in 2023. Frontier markets are trading at close to record-low valuation levels, with a forward-looking P/E ratio of 9.0x, and would also be obvious beneficiaries of falling rates.

Share

Share

Related articles